Overcoming Sri Lanka's payment limitations as an influencer marketplace

Starting and running a digital marketplace in a developing country like Sri Lanka has its challenges. Here's how fluencr overcame them.

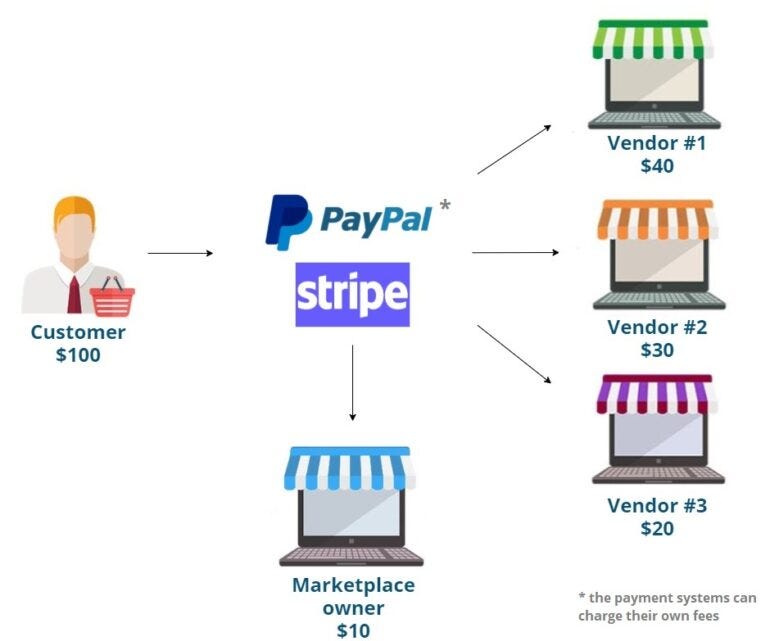

Starting and running a digital business in a developing market like Sri Lanka has its challenges. One of fluencr's key value propositions is how we handle payments. We collect the total campaign payment from the business or agency upfront, hold it until the campaign is over, and then split the payment in order to release it to the respective influencers that were a part of the campaign. This is pretty common in many places, but in Sri Lanka, it's not that simple.

Most countries can use big companies like Stripe or PayPal for a marketplace payments solution, but those options don't work in Sri Lanka. We looked into other global options such as Rapyd, Checkout, Exactly, and Adyen, but none of them were able to facilitate payments in Sri Lanka. We seriously thought about setting up a holding company in Delaware, through Stripe Atlas, all just to get access to Stripe's marketplace payments feature. That's how committed we were to making our product exceptional for our users.

We had to get creative. To overcome this challenge of finding an all-in-one solution that could enable us to capture, hold, and release payments without manual intervention, we decided to break down our payment process into different parts, each handled by a different company.

First, for collecting payments via an IPG, we checked out local providers like PayHere, OnePay, WebxPay, and Marx. Each payment gateway had its own set of challenges. Some couldn't handle payments exceeding Rs. 1M, while others lacked certain features. A few even had pricing models that didn't quite fit our needs. After a thorough comparison of all four vendors, we concluded that Marx was the best fit for us. Their pay-as-you-go model allowed us to use their platform for testing until we were set to launch. However, Marx initially lacked the temporary authorization function (up to 7-day payment holding) and the tokenization feature. Nevertheless, after extensive discussions, they committed to developing these features for us by the time we were ready to launch.

Next, we looked into releasing payments without manual work. We talked to many banks, but they all had separate teams for different things, making it hard to work out a smooth process. Banks, including Sampath Bank, HNB, Commercial Bank, Nations Trust Bank, and NDB surprisingly, all echoed the same sentiment, they didn't have a solution for our needs. Even those that claimed to, like Nations Trust Bank, had a manual element. To make transfers, we had to upload an Excel sheet with the details, and then their team would process it. We extended our inquiries to digital payment options such as Genie, Frimi, LankaPay, and mCash. A special shoutout to the Genie team, who really went the extra mile to help us. Unfortunately, despite their efforts, we didn't find the solution we were looking for.

Meanwhile, we also had conversations with Mastercard and Visa, both of which had their own APIs that could potentially support our needs. However, getting in touch with them and gaining clear insights on how we could implement their solutions turned out to be easier said than done.

We were extremely adamant on making sure we had an end-to-end payments solution that was automated, so settling for anything that had manual intervention, was simply not an option for us.

For a month, it felt like we were stuck. But then, finally, we got a breakthrough. All our persistence paid off. Enter Seylan Bank's digital team, led by the remarkable Vidula. He not only spoke to us but took the time to grasp our unique requirements, showing genuine enthusiasm for our concept. What set Seylan Bank apart was Vidula's revelation that their digital team collaborates seamlessly, their IPG and API teams work cohesively. They confidently assured us that they had precisely what we were in search of. Their IPG could capture the necessary funds, boasting both tokenization and temporary authorization features. They had no qualms about holding funds for us. Additionally, their API, powered by Mastercard, effortlessly released funds to influencers without a hitch. Frankly, we were blown away.

This revelation prompted us to terminate our agreement with Marx, who, regrettably, tried to take advantage of us during the termination process. They did not have the agreed features ready as promised, and they refused to release the refundable deposit which we had paid during set up. For a whole month they dodged our emails until our lawyer had to step in and sort the issue out. We swiftly transitioned to Seylan's payment solution, and it operates flawlessly. Seylan's payment solution seamlessly captures payments, can hold them, and releases them through their API, all without requiring manual intervention.

The key takeaway from this story? Persistence pays off, even when navigating a developing market rife with technological limitations. There's always a solution or a workaround if you look hard enough and work smart enough.